February Pork and Beef Exports Below Year-Ago

February exports of U.S. pork were moderately lower than a year ago, despite continued success in Mexico and Central America, according to data released by USDA and compiled by the U.S. Meat Export Federation (USMEF). February beef exports were also below last year after trending higher in January, while lamb muscle cut exports posted a year-over-year increase for the fifth consecutive month.

February pork exports totaled 241,179 metric tons (mt), down 4% from the large year-ago volume, while value fell 2% to $671.5 million. For the first two months of 2025, pork exports were 3% below last year’s record pace at 485,144 mt, with value down 2% to $1.34 billion.

“I can’t say enough about the tremendous demand for U.S. pork in Mexico and Central America, where the U.S. industry continues to move a wider range of center-of-the-plate cuts to a variety of end users,” said USMEF President and CEO Dan Halstrom. “Unfortunately, the strong performance there has been offset by a slow start to the year in Japan and South Korea. And although February shipments to China were slightly above last year, exports may have been larger if not for the uncertainty over plant eligibility, which wasn’t resolved until mid-March.”

In February and March of this year, many U.S. pork, beef and poultry plants and cold storage facilities were due for a five-year eligibility renewal by China’s General Administration of Customs (GACC). Pork and poultry plants were renewed on the March 16 expiration date, but GACC still has not renewed the eligibility of any U.S. beef establishments, and the majority of U.S. beef production is now ineligible for China.

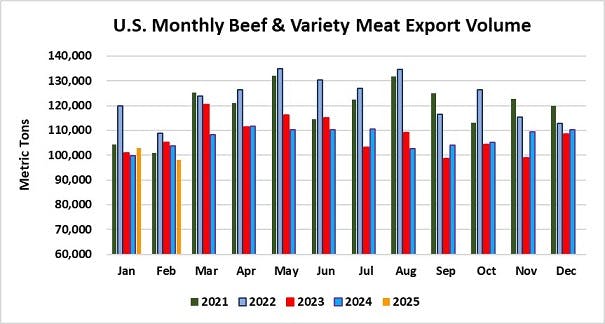

Beef exports totaled 98,198 mt in February, down 5.5% from a year ago, while value declined 4% to just over $800 million. January-February shipments were 1% below last year’s pace at 201,038 mt, but value increased 1% to $1.6 billion.

“It was encouraging to see beef exports to Korea trend higher despite considerable economic and political headwinds, and Canada’s demand for U.S. beef has been very robust to start the year,” Halstrom said. “But exports to China lost momentum in February, likely due in part to the slowdown after Chinese New Year and the questions about plant eligibility. Unfortunately, China has still failed to address the issue of beef plant renewals. This impasse definitely hit our March beef shipments even harder, and the severe impact will continue until China lives up to its commitments under the Phase One Economic and Trade Agreement.”

China also announced additional retaliatory duties, which are summarized in the updated footnotes to this release. This will create further obstacles for U.S. pork and beef exports to China. Halstrom noted that new U.S. tariffs have also created uncertainty for buyers of U.S. red meat in other destinations where retaliation could impact market access and prices.

“USMEF is hopeful that instead of retaliating, other trading partners will choose to lower trade barriers for U.S. exports,” he said. “This would certainly ease the concerns of importers and reduce volatility in the global markets.”

Robust pork demand in Central America and Mexico offset by slowdown in Japan, Korea

Although February pork exports to leading market Mexico saw a slight year-over-year decline in volume (93,178 mt, down 1%), value still climbed 7% to $202.6 million – the eighth consecutive month in which shipments to Mexico have topped $200 million. Through February, pork exports to Mexico were slightly ahead of last year’s record pace in volume (197,680 mt, up 1%) and 7% higher in value ($424.6 million).

Demand for U.S. pork in Central America continues to soar, with February exports up 16% from a year ago to 14,164 mt, while value climbed 18% to $43.3 million. February shipments to Guatemala were the second largest on record at 3,974 mt. These results pushed January-February exports 19% ahead of the record pace of 2024 at 28,674, with value up 24% to $89.9 million, led by robust growth in Honduras, Guatemala and Costa Rica.

February pork exports to China/Hong Kong were 5% higher than a year ago at 38,492 mt, while value was up 8% to $93.1 million. Through February, pork exports to China/Hong Kong were also 5% above last year at 76,088 mt, valued at $185.5 million (up 9%). About two-thirds of the export volume to this region is pork variety meat, although those shipments fell 5% through February to just under 50,000 mt. As noted above, eligibility for export to China was recently renewed for a large number of U.S. pork plants, removing a potential obstacle. However, an additional 10% retaliatory duty on U.S. pork entering China has been in place since March 10. This increased China’s effective tariff rate on U.S. pork to 47%, while most competitors’ products are tariffed at 12%. Effective April 10, China’s total tariff rate on U.S. pork and pork variety meat is set to increase to 81%.

Other January-February results for U.S. pork exports include:

Pork exports to the Philippines reached 4,626 mt in February, up 35% from a year ago, while valued climbed 62% to $11 million. For January through February, exports climbed 20% to 7,771 mt, valued at $17.9 million (up 48%). More than half of this year’s export volume to the Philippines consists of pork variety meat, with those shipments steady with last year at 4,108 mt. The Philippines was last year’s third largest destination for U.S. pork variety meat exports after China/Hong Kong and Mexico.

Cuba’s demand for U.S. pork continued to show promise in February, more than tripling from a year ago to 1,353 mt (up 210% and the second highest on record), while value climbed 259% to just under $4 million. Through February, pork exports to Cuba were up 129% in volume (2,278 mt) and 169% in value ($7.3 million).

February pork exports to New Zealand totaled 864 mt, up 19% from a year ago, while value was up 54% to $3.7 million. Through February, shipments to New Zealand climbed 43% to 1,927 mt, valued at $7.6 million (up 59%). With demand from Australia trending moderately lower than last year’s strong levels, pork exports to Oceania were down 1% to 18,634 mt, while value was 2% below last year’s record pace at $66.4 million.

Pork exports to South Korea were robust during the first half of 2024 but lost momentum later in the year. This trend continued into 2025, with exports through February falling 18% from a year ago to 34,332 mt, with value down 20% to $109.3 million.

Similar to Korea, pork exports to Japan are off to a slow start in 2025. Shipments through February were 19% below last year’s pace in both volume (45,680 mt) and value ($185.7 million).

Pork export value per head slaughtered equated to $66.07 in February, up 6% year-over-year. The January-February average was $61.93 per head, up 1%. Exports accounted for 30.5% of total February pork production and 26.3% of muscle cuts, each up about one percentage point from a year ago. The January-February ratios were fairly steady with last year at 28.7% of total production and 25% for muscle cuts.

Beef exports higher to Korea and Canada; Uncertainty looms for China

February beef exports to leading value market South Korea were slightly above last year at 18,540 mt, while value climbed 4% to $179.8 million. Through February, shipments to Korea edged 1% higher than a year ago at 37,341 mt, while value increased 6% to $362.2 million. Korea’s BSE-related ban on U.S. beef from cattle more than 30 months of age has recently drawn heightened attention from U.S. trade officials.

Removal of this restriction, as well as restrictions on processed beef products, could offer growth opportunities in Korea, especially in a period of tight beef supplies and elevated prices.

Canada’s demand for U.S. beef remained strong in February, with shipments increasing 22% from a year ago to 8,403 mt, while value climbed 21% at $71.1 million. Through February, shipments to Canada were 21% above last year’s pace at 16,860 mt, valued at $137 million.

Beef exports to Egypt, which are mostly beef livers, trended significantly higher than a year ago in February, climbing 15% to 3,390 mt, valued at $6.4 million (up 39%). January-February shipments to Egypt increased 13% to 7,420 mt, while value jumped 36% to $13.7 million. The Middle East’s largest destination for U.S. beef muscle cuts is the United Arab Emirates (UAE), and shipments to the UAE stalled late last year due to halal certification issues. Although January-February exports to the UAE were below last year’s volume, demand rebounded significantly compared to the low totals posted in the fourth quarter of 2024. February shipments to the UAE reached 317 mt, the highest since September. January-February exports to the UAE were 13% higher in value ($10.5 million) despite a 30% decline in volume (625 mt). For the entire Middle East region, January-February exports were slightly above last year’s pace in both volume (9,453 mt, up 3%) and value (just under $40 million, up 2%).

Other January-February results for U.S. beef exports include:

Led primarily by growth in the Philippines, February beef exports to the ASEAN climbed 24% from a year ago to 2,230 mt, valued at $16.6 million (up 4%). Through February, exports to the region were 15% higher in volume (4,091 mt) and 10% higher in value ($32.3 million). While shipments to Indonesia were also above last year’s low volume, market access continues to be problematic. USMEF is working with U.S. trade officials to improve the reliability of the Indonesian market, which is an important destination for short plate and beef variety meat but also holds untapped potential for other muscle cuts. Restoring access to Indonesia is a top priority, especially given heightened trade obstacles in China, which takes a similar mix of products.

Beef exports to Central America have dipped slightly in volume in 2025, falling 2% from last year’s record pace at 3,860 mt. But value has grown impressively, climbing 20% to $32.8 million, led by surging demand in Costa Rica and larger shipments to Guatemala and Panama. February exports to Panama reached the highest monthly value on record at $3.6 million.

Although down from a year ago, January-February beef exports to Mexico remained relatively strong at 37,269 mt (down 7%), valued at $221.8 million (down 5%). Mexico is the largest volume destination for U.S. beef variety meat, and those shipments have trended higher in 2025. Through February, beef variety meat exports to Mexico were up 4% in volume (21,016 mt) and were 5% higher in value ($56.5 million). This included strong increases in exports of beef lips ($15.4 million, up 12%) and hearts ($8.3 million, up 18%).

January-February exports to Japan were down 8% in volume (38,163 mt) and 6% in value ($283.3 million). Beef muscle cut exports to Japan fared better, gaining 2% in value ($228.7 million) despite a 5% decline in volume (32,405 mt). But variety meat exports – mainly tongues and skirts – were sharply lower at 5,758 mt (down 21%), valued at $54.6 million (down 29%). The U.S. is still the leading supplier of tongues to Japan with 42% market share, followed by Australia and Canada. The U.S. holds 75% market share for chilled tongues.

Taiwan’s demand for U.S. beef surged in the second half of last year but has slowed in 2025. Through February, shipments to Taiwan were down 14% from a year ago to 7,126 mt, valued at $87.1 million (down 6%). But on a positive note, Taiwan’s imports of U.S. chilled beef increased 13% through February, reaching 3,842 mt, and capturing 73% market share.

Beef exports to China/Hong Kong trended lower in February, falling 15% from a year ago to 15,415 mt, valued at $135.5 million (down 19%). Because of a strong January performance, exports through February were still 5% above last year at 34,173 mt, though value fell slightly to $298.5 million. Even more concerning is the fate of U.S. exports to China moving forward, due to the aforementioned delay in China’s renewal of beef plant registrations. China also imposed an additional 10% retaliatory duty on U.S. beef on March 10, raising the effective tariff rate to 22%. Effective April 10, China’s total duty rate is set to increase to 56%. U.S. beef’s primary competitor in China – grain-fed beef from Australia – enjoys duty-free access under a bilateral trade agreement. New Zealand beef is also duty-free, while most other suppliers are tariffed at 12%.

Beef export value per head of fed slaughter equated to $432.90 in February, up 5% year-over-year. The January-February average was $399.34 per head, up 3.5%. Exports accounted for a record 14.2% of total February beef production and 11.9% for muscle cuts, each slightly higher than a year ago. The January-February ratios were 13.4% of total production and 10.9% for muscle cuts, compared to 13.3% and 11.1%, respectively, during the same period last year.

Mexico’s demand for U.S. lamb cuts continues to expand

February exports of U.S. lamb muscle cuts totaled 214 mt, up 42% from a year ago, valued at $1.12 million (up 13%). Growth was led by Mexico, where shipments climbed 133% to 126 mt, valued at just over $400,000 (up 135%). For the second consecutive month, export volume to Mexico was the highest since November 2022. January-February exports to all destinations increased 17% in volume (469 mt) and 6% in value ($2.6 million). With a wider range of lamb cuts – including shoulder and flap meat – gaining popularity in Mexico’s foodservice sector, January-February exports to Mexico climbed 55% to 246 mt, valued at $856,000. Shipments to the Caribbean also trended higher, led by growth in Trinidad and Tobago and the Leeward-Windward Islands.

Complete January-February export results for U.S. pork, beef and lamb are available from USMEF’s statistics web page.

For questions, please contact Joe Schuele or call 303-547-0030.

NOTES:

Export statistics refer to both muscle cuts and variety meat, unless otherwise noted.

One metric ton (mt) = 2,204.622 pounds.

U.S. pork and beef currently face retaliatory duties in China. In February 2020, China announced a duty exclusion process that allows importers to apply for relief from duties imposed in response to U.S. Section 301 duties. When an application is successful, the rate for U.S. beef can decline to the MFN rate of 12% and the rate for U.S. pork can decline to 37% (the MFN rate plus the 25% Section 232 retaliatory duty, which remains in place). But China imposed an additional 10% retaliatory duty on U.S. pork and beef on March 10, 2025, and additional retaliatory duties were announced in April 2025. China’s new retaliatory duties were first announced at 34% but were later increased to 84% and further increased to 125%. The additional tariffs pushed China’s effective duty rate on U.S. pork and pork variety meat to 172% and beef and beef variety meat are now tariffed at 147%. These rates represent the sum total of China’s 12% most-favored-nation tariff, plus retaliatory duties previously imposed by China, plus all recently announced retaliatory duties.